How Compounding Works in Investing: A Simple Step-by-Step Explanation

In practical terms, compounding is the single habit that separates small, short-lived gains from sustained wealth accumulation. From what I’ve seen over many years working with investors, the mechanics are simple — but the discipline to exploit them is not. This article explains how compounding works in investing in plain English, shows worked examples in $, compares time horizons, and gives practical, actionable rules you can use today.

You will learn:

- What compounding means in investment and how it differs from simple interest.

- A step-by-step breakdown of how compounding grows money.

- Clear numerical examples for 5, 10 and 20 years.

- How compounding works in SIPs, mutual funds, stocks and fixed deposits.

- How to maximise compounding and the common mistakes that kill it.

- Answers to common questions (FAQs) investors actually search for.

This is experience-based, practical guidance — not textbook fluff. I’ll mention financekd.com where it helps explain real application and authority.

What Is Compounding in Investing? (Simple Definition for Beginners)

Compounding meaning in investing (no maths, plain English)

Compounding, in investing, means your investment’s returns are reinvested so they themselves earn returns. In plain English: you earn returns on both the money you put in (the principal) and the returns that money has already produced. That “interest on interest” effect is compounding.

Why compounding is called the “8th Wonder of the World”

Albert Einstein reportedly called compound interest the “eighth wonder of the world” because of its exponential effect. In practical terms, the longer you leave rewards to accumulate, the larger the gains — often far exceeding additional contributions. This is not magic; it’s mathematics combined with time and reinvestment discipline.

Difference between compounding and simple interest

- Simple interest: you earn interest only on the original principal. $1,000 at 5% simple interest gives $50 per year — always $50.

- Compounding: interest is added to the principal and future interest calculations include that added interest. That same $1,000 at 5% compounded annually gives increasing dollars each year because the base grows.

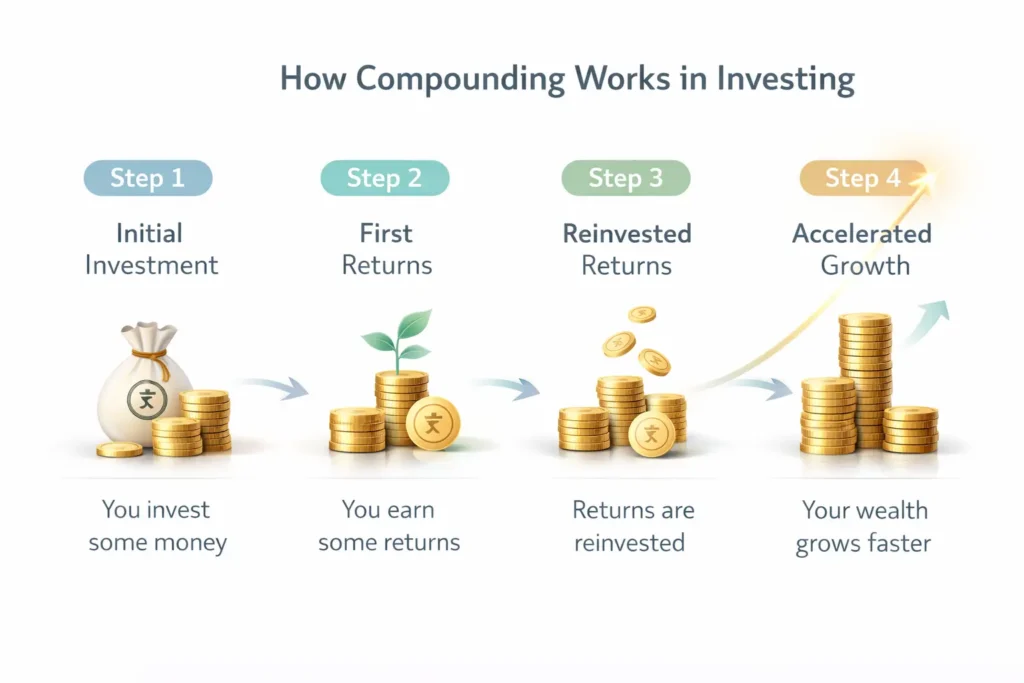

How Compounding Works – Step-by-Step Explanation

(Core ranking section — read carefully; this is where the concept becomes practical.)

Step 1 – You Invest Your Initial Amount (Principal)

In practice, everything starts with the investment principal — the amount you put to work.

Example (simple): You invest $1,000 today. That is your starting principal.

Step 2 – You Earn Returns on Your Investment

Your investment generates returns. These returns could be interest, dividends, capital gains, or reinvested distributions. The annual rate of return matters: 6%, 8%, 10% — small differences compound into large outcome gaps over time.

Example: At a 10% annual return, $1,000 becomes $1,100 after one year.

Step 3 – Returns Start Earning Returns (Compounding Effect)

Here is the key moment: at year two, you’re not earning return only on the original $1,000 — you earn return on $1,100. That extra $100 now earns its own return. That is interest on interest.

Example: Year two at 10%: $1,100 × 1.10 = $1,210.

Step 4 – Time Multiplies Your Money Automatically

Compounding’s force is time. The longer you remain invested and continuously reinvest returns, the larger the multiplication effect. This is why compounding requires patience, not market timing. Markets fluctuate; compounding favours consistency.

In practical terms: consistent reinvestment + time = exponential growth.

Simple Compounding Example (With Easy Numbers)

Below are worked examples showing how compounding affects growth over different time horizons. All examples assume annual compounding and returns reinvested.

Compounding example for 5 years

Assumptions:

- Initial principal: $1,000

- Annual rate: 8%

- Compounding: annually

Calculation:

- Year 1: $1,000 × 1.08 = $1,080

- Year 2: $1,080 × 1.08 = $1,166.40

- Year 3: $1,166.40 × 1.08 = $1,259.71

- Year 4: $1,259.71 × 1.08 = $1,360.49

- Year 5: $1,360.49 × 1.08 = $1,469.33

Total after 5 years: $1,469.33 (approx)

Compounding example for 10 years

Same inputs:

- After 10 years at 8%: Final amount = $1,000 × (1.08)^10 ≈ $2,158.92

Compounding example for 20 years

- After 20 years at 8%: Final amount = $1,000 × (1.08)^20 ≈ $4,660.96

Table: Compounding growth (annual compounding)

| Years | Growth Factor (1.08^n) | Final Amount on $1,000 |

|---|---|---|

| 5 | 1.4693 | $1,469.33 |

| 10 | 2.1589 | $2,158.92 |

| 20 | 4.66096 | $4,660.96 |

This table demonstrates the exponential effect: doubling time at 8% is roughly 9 years (Rule of 72: 72 / rate ≈ doubling years).

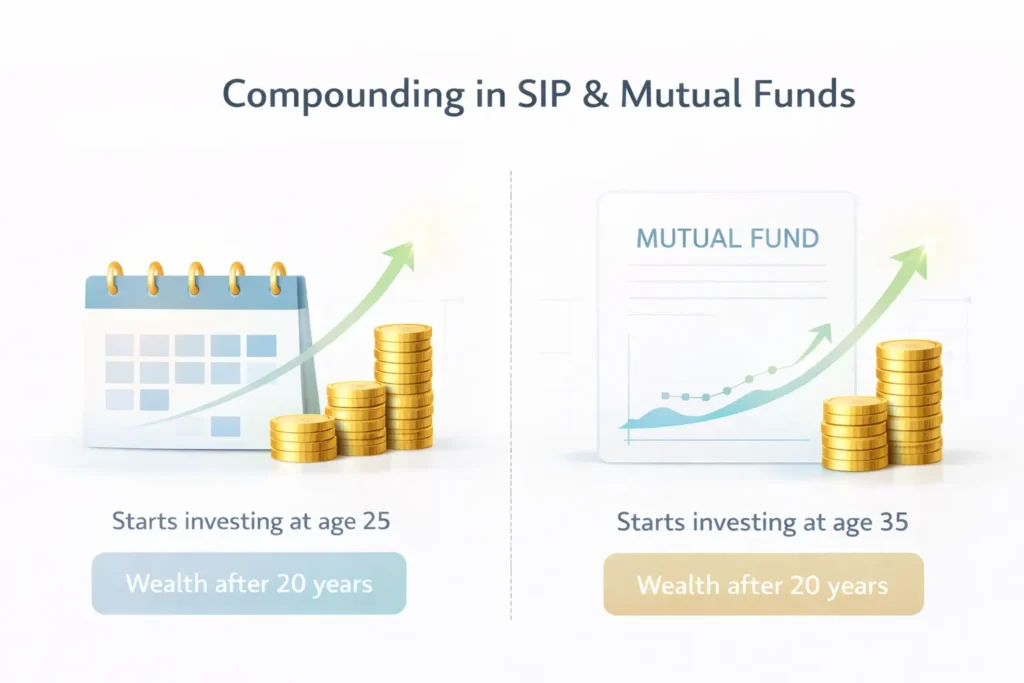

Power of Compounding Over Time (Why Early Investing Wins)

Investing early vs investing late (comparison)

Two investors:

- Alice invests $200 per month from age 25 to 35 (10 years), then stops and never adds again; she leaves the money invested until 65.

- Ben starts at 35 and invests $200 per month until 65 (30 years).

At the same annual return, Alice’s early head start often beats Ben’s longer contributions. In practical terms, early investing leverages more compounding years.

How time matters more than amount invested

Time is multiplicative; additional contributions help, but time compounds every single dollar more powerfully. Most people don’t realise that a small regular amount started early often outperforms larger late contributions.

Small monthly investments → big long-term wealth

Even modest monthly investments compound surprisingly well. For example, $100 per month at 8% for 30 years grows to approximately $128,000.

Compounding in SIP, Mutual Funds, Stocks & FD

How Compounding Works in SIP Investments

SIP (Systematic Investment Plan) compounds via regular contributions and reinvestment of returns in mutual funds. In practical terms, you buy units each month; those units may grow (NAV increase) and distributions may be reinvested, causing compounding.

Example: $100 monthly SIP at 10% annualised over 20 years ≈ substantial wealth due to both contributions and reinvested gains.

Compounding in Mutual Funds

Mutual fund returns (NAV appreciation + dividend reinvestment) create compounding. For equity mutual funds, capital gains and dividend reinvestments fuel compounding; for bond funds, interest reinvested adds up.

Compounding in Stock Market

Compounding in the stock market often comes from:

- Reinvested dividends

- Capital gains that remain invested

- Dividend growth over time (if company increases dividend, reinvestment buys more shares)

Stocks can compound powerfully but with greater volatility.

Compounding in Fixed Deposits (FD)

Fixed deposits (time deposits) compound according to the stated compounding frequency — annually, quarterly, monthly or daily. A higher compounding frequency slightly increases effective yield. For FDs, compounding is predictable; for equities and funds it’s variable.

Compounding Frequency Explained (Daily, Monthly, Yearly)

What is compounding frequency?

Compounding frequency refers to how often returns are added to the principal. Common frequencies: annually, semi-annually, quarterly, monthly, daily. More frequent compounding produces marginally higher returns if the nominal rate is unchanged.

Daily vs monthly vs yearly compounding – which is better?

All else equal, more frequent compounding is better. However, the incremental benefit diminishes. For example, 8% compounded annually vs 8% compounded monthly yields a small difference in effective annual yield.

Does higher compounding frequency always mean higher returns?

Only if the nominal rate is the same. In real markets, instruments with higher compounding frequency may have different rates or risks. For practical investing, focus more on rate of return and reinvestment opportunity than micro differences in frequency.

Common Mistakes That Kill Compounding Returns

This section matters more than people expect. From what I’ve seen, these errors are common and costly.

Stopping investments too early

Pausing contributions or liquidating early interrupts compounding. Compounding rewards continuous reinvestment.

Withdrawing profits frequently

Taking out gains means those gains stop compounding. If you need cash, aim to keep the invested principal compounding and withdraw only small, planned amounts.

Chasing short-term returns

Switching funds frequently after chasing top performers resets your compounding clock and often increases costs (taxes, fees), which reduce compounding returns.

Ignoring inflation and taxes

Nominal compounding can look attractive; real compounding (after inflation and tax) is what builds purchasing power. Long term equity investing tends to beat inflation if chosen sensibly.

How to Maximise the Power of Compounding (Proven Tips)

Start early, even with small amounts

Starting earlier is the single most powerful lever. Small sums at a young age can exceed larger sums invested later.

Stay invested during market crashes

In practical terms, market downturns are compounding opportunities — you buy assets at lower prices; when markets recover, those cheaper units compound more.

Increase investment amount gradually

Raise contributions with income growth. A 1–2% annual increase in contributions has a powerful cumulative effect.

Reinvest all returns

Automatic reinvestment of dividends, interest and distributions is essential. Reinvesting keeps the compounding loop intact.

Compounding vs Inflation – Does Compounding Beat Inflation?

Real returns explained simply

Real return = nominal return − inflation − taxes − fees. Compounding beats inflation when your real return is positive over time. Equity and inflation-linked investments are commonly used to preserve real purchasing power.

Why long-term equity helps beat inflation

Equities tend to grow companies’ earnings and dividends over time — this supports long-term capital growth above inflation. For compounding to beat inflation, choose assets and strategies that historically provide positive real returns.

How Long Does Compounding Take to Show Results?

Investors often ask: “How much time does compounding need?”

First 5 years – slow phase

The early years are steady but not spectacular; returns mainly rebuild the principal base.

Next 10 years – acceleration phase

Once your compounded base grows, returns accelerate — you start to notice clearer gains.

Final years – wealth explosion phase

After several decades, the curve steepens dramatically, especially with above-average rates and continued contributions.

In practical terms: patience is not a virtue in investing — it is a necessity.

Is Compounding Safe? Risks You Should Know

Market risk vs compounding logic

Compounding is a mechanism; it does not eliminate market risk. Investments can shrink. The compounding effect multiplies both gains and losses.

How diversification protects compounding

Diversification reduces unsystematic risk and protects the compounding process from catastrophic single-investment failure. A diversified portfolio smooths returns and preserves the compound base.

Worked Examples & Tables — Practical Scenarios

Example A — Lump Sum compounding at different rates

Assumptions:

- Principal: $10,000

- Rates: 6%, 8%, 10%

- Periods: 5, 10, 20 years

| Years | 6% ($) | 8% ($) | 10% ($) |

|---|---|---|---|

| 5 | 13,382 | 14,693 | 16,105 |

| 10 | 17,908 | 21,589 | 25,937 |

| 20 | 32,071 | 46,610 | 67,275 |

Example B — SIP / Monthly investment compounding

Assumptions:

- Monthly contribution: $200

- Annual return: 8% (monthly equivalent)

- Periods: 10, 20, 30 years

| Years | Total Invested ($) | Final Amount ($) |

|---|---|---|

| 10 | 24,000 | ~33,348 |

| 20 | 48,000 | ~92,992 |

| 30 | 72,000 | ~205,000 |

Note: These are approximate values using a monthly compounding formula. The key point: contributions are modest relative to final amount because of compounding.

Compounding Worked Example: How compounding works over 10 years (detailed)

Assume:

- Principal: $5,000

- Annual return: 9% (equity-like)

- No further contributions

Using formula: Future Value = Principal × (1 + r)^n

$5,000 × (1.09)^10 ≈ $11,834

If you added $100 monthly for 10 years at 9%:

- Monthly r ≈ 0.75%

Future value ≈ $16,700 (approx) — illustrating that monthly contributions accelerate compounding.

FAQs About Compounding in Investing

What is compounding in investing?

Compounding in investing is the process where the returns you earn on an investment are reinvested so they begin to generate their own returns over time. Instead of earning returns only on your original amount, you earn returns on both the principal and the accumulated gains. In practical terms, this reinvestment creates exponential growth, making time the most powerful factor in long-term wealth building.

How does compounding help investors?

Compounding helps investors by allowing their investment returns to be reinvested so those returns start earning additional returns over time. In practical terms, money grows faster as the investment base increases each year, even without adding new funds. This long-term reinvestment effect turns small, regular investments into substantial wealth and rewards patience and consistency.

How long does compounding take to work?

Compounding takes time to work, and its impact is not immediate. In the first few years, growth appears slow because returns are calculated on a small base. From around 7–10 years, compounding becomes more visible as returns start earning returns. Over longer periods, especially 15–20 years, the effect accelerates significantly and drives substantial wealth growth.

Is compounding guaranteed?

Compounding is not guaranteed in investing. Compounding is a mathematical effect that works only when investment returns are positive and consistently reinvested. Market fluctuations, losses, inflation, taxes, and early withdrawals can interrupt or reduce compounding. While the concept is reliable, actual results depend on investment performance, time horizon, and disciplined long-term investing.

Can compounding make you rich?

Compounding, combined with time, discipline and adequate returns, can generate substantial wealth. It is not a guarantee of riches but it is the most reliable mechanism for wealth accumulation.

What investment gives best compounding?

Historically, equities (direct stocks or equity mutual funds) have provided high long-term compounding potential, but they carry risk. Diversified portfolios that reinvest earnings are practical compounding vehicles.

How much should I invest to benefit from compounding?

There is no fixed minimum amount required to benefit from compounding. In practical terms, even small, regular investments can compound effectively if they are started early and left invested for a long period. What matters most is consistency, reinvestment of returns, and time. The earlier you begin, the greater the compounding benefit—regardless of the initial amount.

How does compounding work with investing?

Compounding in investing works by reinvesting your returns so they generate additional returns over time. Instead of earning returns only on your original investment, you earn returns on both the principal and past gains. In practical terms, the longer you stay invested and reinvest earnings, the faster your wealth grows due to exponential growth.

How much is $10,000 worth in 10 years at 5% annual interest?

At a 5% annual compounded return, $10,000 grows to approximately $16,289 in 10 years. This growth happens because each year’s interest is added to the principal, allowing future interest to be calculated on a higher amount. Compounding rewards time more than frequent contributions.

What is the 7-5-3-1 rule in SIP?

The 7-5-3-1 rule in SIP is a time-based investment guideline. It suggests equity investments need at least 7 years for stability, 5 years for decent returns, 3 years to recover from volatility, and 1 year is too short for equity SIPs. It highlights why long-term investing is essential.

What is $5,000 invested for 10 years at 10% compounded annually?

If $5,000 is invested at 10% compounded annually for 10 years, it grows to approximately $12,968. This happens because returns are reinvested each year, allowing interest to earn further interest. Over longer periods, compounding significantly accelerates investment growth.

Which bank gives 9.5% interest?

Interest rates vary by country, account type, and time period. Some banks may offer close to 9.5% interest on special fixed deposits, senior citizen schemes, or promotional term deposits. However, such rates are usually time-limited and come with conditions. Always compare rates, lock-in periods, and inflation impact before investing.

How to turn $10K into $100K in 10 years?

Turning $10,000 into $100,000 in 10 years requires a high annual return of roughly 26%, which involves significant risk. This is typically possible only through aggressive equity investing, business ownership, or high-growth assets. Most long-term investors rely on compounding over longer periods with realistic returns.

What are the risks of compound interest?

The main risks of compound interest come from market volatility, inflation, taxes, and early withdrawals. Compounding works best when returns are consistently reinvested. Poor investment choices or frequent withdrawals can reduce or even reverse compounding benefits. Diversification and long-term discipline help manage these risks.

Final Thoughts – Why Compounding Is the Key to Long-Term Wealth

From what I’ve seen, compounding is not clever math; it’s a behavioural advantage. The investor who starts early, reinvests returns, and resists the urge to tinker will almost always outpace the investor who chases short-term gains.

Actionable summary:

- Start as soon as you can — even modest sums.

- Reinvest returns automatically.

- Keep costs and taxes low.

- Stay diversified.

- Increase contributions over time.

If you’re ready to put this into practice, open a systematic investment plan, set up automatic reinvestment and let time do the heavy lifting. For practical guides, calculators and deeper walkthroughs tailored for different risk profiles, visit financekd.com — I’ve written practical tools and examples there to help you start.

Begin today: compounding rewards the patient and the disciplined.