How Do Banks Calculate Loan Eligibility

Introduction

How do banks calculate loan eligibility? It’s one of the most common questions I hear from borrowers who are ready to take a loan but unsure how much they’ll actually get approved for.

In practical terms, loan eligibility isn’t just about how much you earn. Banks look deeper—at income stability, repayment capacity, existing obligations, and how responsibly you’ve handled credit in the past. This is where many borrowers go wrong. They assume eligibility equals income × some random number.

From what I’ve seen over the years, understanding how banks calculate loan eligibility before applying can save you from rejections, credit score damage, and disappointment.

In this guide, I’ll break down the loan eligibility calculation process explained step by step, using real-world logic banks actually follow in the USA.

What Is Loan Eligibility and Why It Matters?

Loan eligibility refers to the maximum loan amount a bank is willing to approve based on your financial profile.

Most people don’t realise that:

- Eligibility ≠ loan applied amount

- Eligibility ≠ what your friend got

- Eligibility ≠ what online calculators promise

Why banks calculate eligibility

Banks calculate loan eligibility to:

- Reduce default risk

- Ensure long-term affordability

- Match repayments with income stability

This is part of a broader affordability assessment and repayment capacity analysis.

Why approved amount is often lower than expected

In real life, banks apply buffers. Even if numbers look fine on paper, underwriters factor in:

- Lifestyle expenses

- Future rate hikes

- Income volatility

That’s why loan eligibility calculation explained online often differs from actual approvals.

How Do Banks Decide How Much You Can Borrow?

When people ask “how banks decide loan amount”, the honest answer is: risk first, income second.

Banks don’t start with:

“How much can we lend?”

They start with:

“How safely can this person repay for years?”

Core underwriting logic

Banks assess:

- Disposable income calculation

- Debt servicing capacity

- Cash-flow evaluation

- Credit behaviour patterns

Even if your income supports a higher EMI, banks may approve less to stay within policy limits.

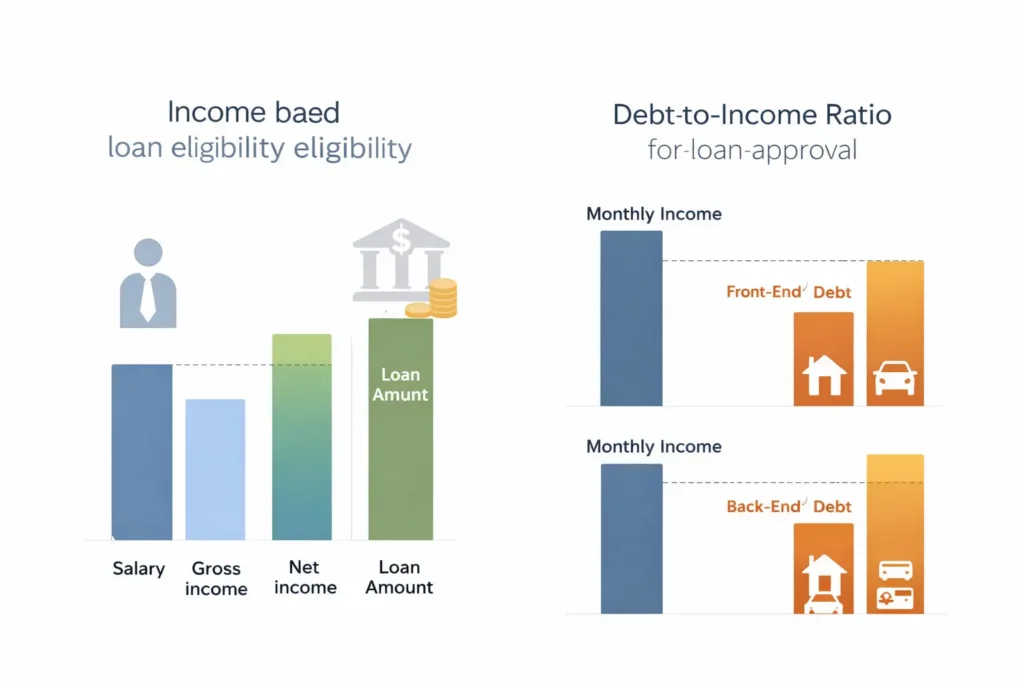

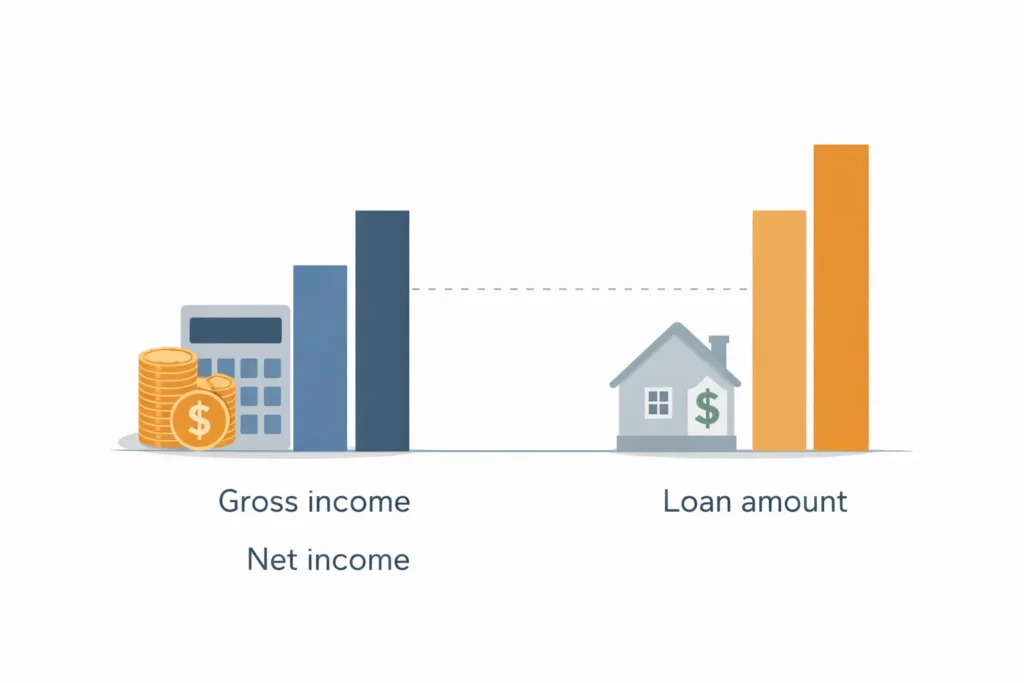

Loan Eligibility Based on Income (USA Explained)

Income is the foundation, but not all income is treated equally.

How Banks Calculate Loan Eligibility Based on Salary

Banks look at:

- Monthly vs annual income

- Gross vs net income for loan

- Verified income calculation

For salaried borrowers:

- Net monthly income matters more than CTC

- Consistency matters more than bonuses

For self-employed borrowers:

- Average income over 2–3 years

- Tax returns + bank statements

- Earnings consistency review

Income Stability Banks Look For

Income stability assessment includes:

- Job tenure (usually 12–24 months)

- Industry risk (tech, retail, healthcare vary)

- Variable income haircut (commissions, freelance)

Example:

- $60,000 annual income → lower buffer

- $80,000 stable income → higher eligibility

But stability beats higher numbers every time.

Debt-to-Income (DTI) Ratio Explained for Loan Approval

DTI is non-negotiable in the USA.

What Is DTI Ratio?

DTI = Total monthly debt payments ÷ Gross monthly income

Banks check:

- Front-end DTI (housing only)

- Back-end DTI (all debts combined)

Ideal DTI Ratio for Loan Approval

| DTI Ratio | Bank View |

|---|---|

| Below 30% | Excellent |

| 31–36% | Safe |

| 37–43% | Borderline |

| Above 43% | High risk |

Even high earners get rejected here.

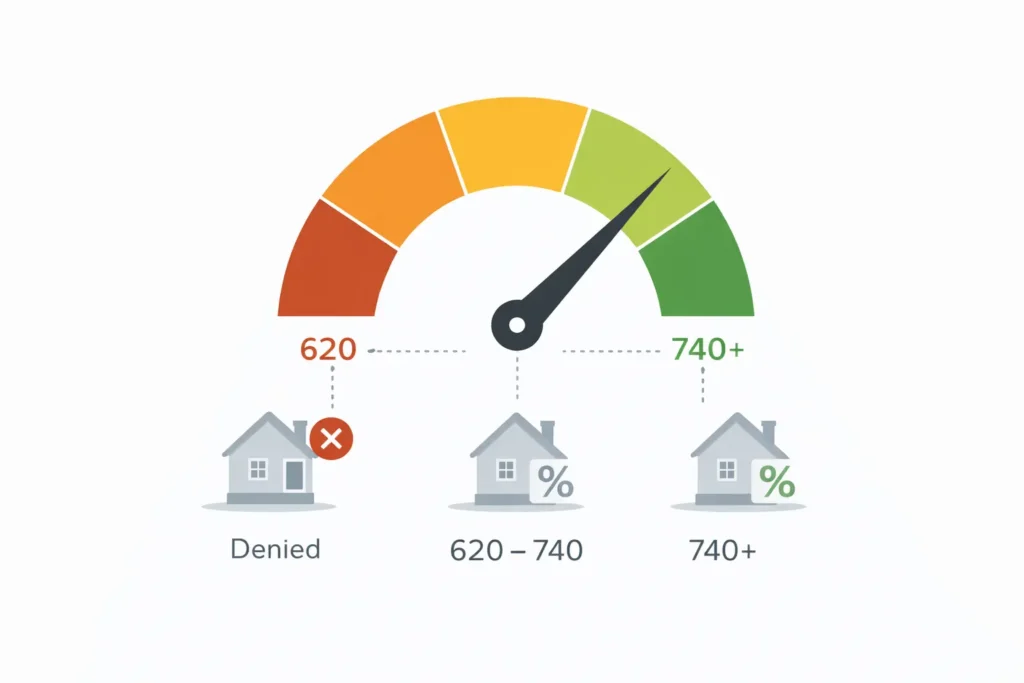

How Credit Score Affects Loan Eligibility

Credit score doesn’t just affect approval—it affects how much loan you can get.

Credit Score Ranges and Loan Impact

- 620–679: Limited eligibility, higher interest

- 680–739: Normal approval range

- 740+: Best rates, higher approval limits

From what I’ve seen, a strong credit score allows banks to stretch eligibility slightly—but it never overrides poor cash flow.

Other Factors Banks Consider Before Approving a Loan

Beyond income and DTI, banks also review:

- Existing loans and credit cards

- Loan tenure (longer tenure = higher eligibility)

- Loan type (personal vs mortgage)

- Down payment size (for home loans)

This is part of overall affordability assessment, not just numbers.

Mortgage vs Personal Loan Eligibility – Key Differences

Mortgage rules are stricter—but more flexible long term.

Key differences:

- Mortgage allows higher DTI

- Longer tenure improves eligibility

- Property acts as collateral

Personal loans rely heavily on income stability requirements and credit score.

Why Banks Approve Lower Loan Amount Than Expected

This frustrates borrowers the most.

Banks reduce amounts due to:

- Internal risk buffers

- Policy-level caps

- Credit history inconsistencies

Most people don’t realise banks plan for future uncertainty, not present comfort.

Loan Pre-Approval vs Final Approval – Important Difference

Pre-approval is conditional.

Final approval depends on:

- Income verification standards

- Bank statement review

- Employment confirmation

Many pre-approved loans fail here.

How Banks Verify Income for Loan Approval

Verification is strict.

Banks usually ask for:

- Recent pay stubs

- Tax returns (W-2 / 1099)

- Bank statements

For self-employed:

- Business income proof

- Cash-flow analysis

- Earnings consistency

Any mismatch raises red flags.

Frequently Asked Questions (PAA Optimised)

How much loan can I get with $60,000 salary?

Typically, eligibility ranges from 4–6× annual income, adjusted for DTI and existing debt. Strong credit and low obligations improve approval chances.

How much loan can I get with $80,000 income?

With an $80,000 annual income, the loan amount you can get mainly depends on your Debt-to-Income (DTI) ratio, credit score, and loan type—not just income.

In practical terms:

- If your DTI is below 36% and credit score is 700+

→ You may qualify for 4–6× your annual income

Typical estimates (USA):

- Personal loan: ~$20,000 – $50,000

- Auto loan: ~$30,000 – $60,000

- Mortgage: ~$300,000 – $420,000 (longer tenure + property collateral)

From what I’ve seen, borrowers with low existing debt and stable income usually get closer to the higher end. High EMIs or recent credit usage can pull this down quickly.

Can banks deny loan even with good credit?

Yes. Poor cash flow, high DTI, or unstable income can override a good credit score.

Does existing debt affect loan eligibility?

Banks look at your total monthly obligations—credit card EMIs, personal loans, auto loans, education loans—and calculate your Debt-to-Income (DTI) ratio.

If a large portion of your income is already committed, your repayment capacity falls, and banks either reduce the loan amount or reject the application, even with a good credit score.

How is loan eligibility calculated?

Loan eligibility is calculated using your monthly income, existing EMIs, credit score, and repayment capacity. Banks assess disposable income after expenses, apply a safe EMI limit (usually 40–50% of income), and adjust the final loan amount based on risk, tenure, and credit history.

How do banks determine if you qualify for a loan?

Banks determine loan qualification by checking income stability, debt-to-income ratio, credit score, existing liabilities, and repayment history. Even with good income, high EMIs or inconsistent earnings can reduce approval chances. Qualification is based on affordability, not just salary.

Who is eligible for a Personal Loan on ₹70,000 salary?

With a ₹70,000 monthly salary, salaried individuals with stable employment, low existing EMIs, and a credit score above 700 are usually eligible. Banks typically allow EMIs up to 40–50% of income, which directly determines the personal loan amount you qualify for.

What is the 5-20-30-40 rule for home loan?

The 5-20-30-40 rule means: 5 years minimum job stability, 20% down payment, 30 years maximum loan tenure, and EMIs capped at 40% of monthly income. This rule helps banks ensure long-term affordability and reduces default risk.

How much Personal Loan can I get if my salary is ₹60,000?

If your salary is ₹60,000 per month, banks may approve a personal loan where the EMI does not exceed ₹25,000–₹30,000. The final loan amount depends on tenure, interest rate, existing debts, and credit score, typically ranging between ₹6–10 lakhs.

What are the 5 keys to qualify for a loan?

The five key factors are stable income, good credit score, low existing debt, consistent repayment history, and sufficient income after expenses. Banks prioritise repayment capacity and cash flow stability more than just salary size when approving loans.

Can I get a housing loan of ₹40 lakhs if my salary is ₹55,000?

With a ₹55,000 salary, a ₹40 lakh home loan is difficult unless there is a co-applicant or longer tenure. Banks usually cap EMIs at 40–50% of income, which limits the eligible loan amount unless additional income support exists.

What are red flags in the loan process?

Red flags include frequent job changes, high credit card usage, delayed EMIs, low bank balance, unexplained cash deposits, and multiple recent loan enquiries. These signals suggest higher risk and often lead banks to reduce loan amount or reject the application.

How much loan can I get for ₹18,000 salary?

With a ₹18,000 monthly salary, loan eligibility is limited. Banks may allow EMIs up to ₹7,000–₹8,000, resulting in a small personal loan depending on tenure and interest rate. Credit score and existing obligations play a critical role here.

How much home loan can I get if my salary is ₹70,000?

For a ₹70,000 salary, banks generally allow EMIs up to ₹30,000–₹35,000. Based on tenure and interest rate, this may translate into a home loan of approximately ₹35–50 lakhs, subject to credit score and existing liabilities.

What are common reasons for loan denial?

Common reasons include high existing EMIs, low credit score, unstable income, frequent job changes, poor repayment history, and incorrect income documents. Even high earners face rejection if affordability and cash-flow checks fail.

Is 720 a good CIBIL score for a Personal Loan?

Yes, a 720 CIBIL score is considered good for a personal loan. It improves approval chances and may help secure better interest rates. However, banks still evaluate income stability, EMI burden, and repayment capacity before final approval.

Conclusion

At the end of the day, loan eligibility is a balance, not a formula.

Banks calculate eligibility using:

- Income stability

- Repayment capacity

- DTI ratio

- Credit behaviour

Planning before applying—reducing debt, stabilising income, and understanding your limits—can dramatically improve approval chances.

From what I’ve seen, borrowers who prepare before applying almost always get better results than those who rush.

If you want more practical finance guidance like this, explore in-depth articles on financekd.com, where real-world money decisions are explained clearly—without fluff.