Introduction – What is the 7-5-3-1 Rule in SIP?

What is the 7-5-3-1 Rule in SIP? This is a question many investors only start asking after they have already made costly mistakes. From what I have seen over the last several years, SIP failures in India almost never happen because mutual funds are flawed products. They happen because investors misunderstand time, underestimate risk, and overestimate their own emotional tolerance during market volatility.

In practical terms, the SIP journey usually begins with optimism. A Systematic Investment Plan (SIP) is started after watching a market rally, hearing a colleague’s success story, or receiving advice from a relationship manager. The first few months feel reassuring. NAVs move up, portfolio statements look healthy, and confidence grows. At this stage, SIP investing appears simple and rewarding.

Then reality intervenes.

Markets correct. Sometimes sharply. News channels flash words like crash, sell-off, and global uncertainty. Social media fills with fear-driven predictions. Suddenly, the same SIP that was labelled “long-term” begins to feel uncomfortable. Doubts creep in. Questions like “Should I stop?” or “Should I withdraw now and re-enter later?” start dominating the investor’s mind.

This is where many SIP investors go wrong—not because the investment was wrong, but because the investment was never aligned with the correct time horizon.

Most people don’t realise that returns should never be the starting point of SIP planning. Chasing past performance charts without understanding risk exposure is one of the biggest reasons investors exit at the worst possible time. Short-term money is often invested in equity, while long-term goals are pursued without any clear structure or risk control. The result is emotional decision-making, panic selling, and disappointment.

The 7-5-3-1 rule in SIP was designed to correct this exact behavioural flaw. It is a time-based investment framework that connects when you need your money with how that money should be invested. By clearly separating long-term growth goals from medium- and short-term needs, this rule brings discipline, clarity, and safety into mutual fund investing.

For salaried individuals, first-time investors, and anyone who values financial security over speculation, the 7-5-3-1 rule acts as a practical guardrail. It does not promise extraordinary returns. Instead, it helps investors stay invested through market cycles, reduce emotional stress, and build wealth in a structured, sustainable way.

What is the 7-5-3-1 Rule in SIP? (Simple Explanation)

The 7-5-3-1 rule in SIP is a time-based SIP investment framework. It connects how long you can stay invested with what type of mutual fund you should choose.

Instead of asking:

“Which mutual fund gives the highest return?”

It asks a smarter question:

“When will I actually need this money?”

The rule works like this:

- 7 years or more → Equity mutual funds

- 5 years → Hybrid (equity + debt) mutual funds

- 3 years → Debt mutual funds

- 1 year → Liquid or ultra-short-term funds

The logic behind these numbers is not random. It is based on market cycles, volatility behaviour, and risk-adjusted returns.

In simple words, the longer your investment horizon, the more risk you can afford. The shorter the horizon, the more stability you need.

That is the real 7 5 3 1 SIP rule meaning—not chasing returns, but matching risk with time.

Meaning of the 7-5-3-1 Rule in SIP

7-Year Rule – Equity Mutual Funds for Long-Term Wealth

Equity mutual funds are powerful—but only if given enough time.

From what I have seen, equity markets rarely move in straight lines. There are rallies, crashes, sideways phases, and sudden shocks. Over short periods, equity can feel unpredictable. Over 7 years or more, however, the story changes.

Market cycles tend to complete themselves. Bad years are often followed by strong recoveries. Volatility smoothens out.

This is why the 7-year rule exists.

Equity SIPs are best suited for:

- Retirement planning

- Child’s higher education

- Long-term wealth creation

- Financial independence goals

In practical terms, if you cannot mentally tolerate seeing your investment fall 20–30% at some point, equity SIPs should not be used for that goal.

5-Year Rule – Hybrid Funds for Balanced Growth

Five years is a tricky time horizon. Too long for pure debt, yet not long enough for full equity exposure.

This is where hybrid mutual funds play a crucial role.

Hybrid funds combine equity and debt in varying proportions. When markets rise, equity fuels growth. When markets fall, debt cushions the impact.

From what I have observed, investors using hybrid funds panic far less during market corrections. That emotional stability alone improves long-term outcomes.

Ideal goals for 5-year SIPs include:

- House down payment

- Business expansion planning

- Medium-term capital goals

This section of the 7-5-3-1 rule in SIP explained properly often saves investors from costly mistakes.

3-Year Rule – Debt Funds for Capital Protection

Three-year goals should never be exposed to equity risk.

This is one of the most common mistakes Indian investors make—investing short-term money in equity hoping for quick gains.

Debt funds are designed for capital protection with modest growth. They invest in government securities, corporate bonds, and money market instruments.

In practical terms, debt funds aim to protect your money while offering returns that can be more tax-efficient than fixed deposits in some cases.

Typical 3-year goals:

- Car purchase

- Wedding expenses

- Planned business investments

This is a core part of a SIP risk management strategy.

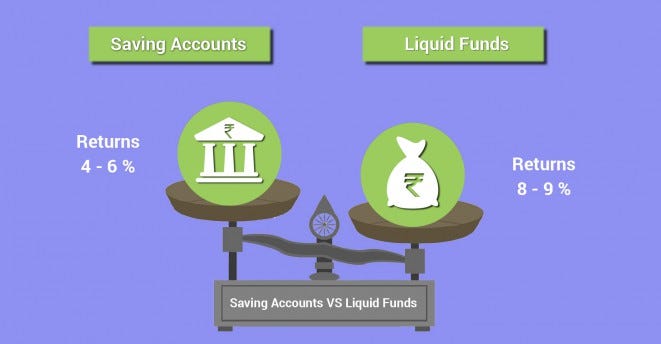

1-Year Rule – Liquid Funds for Safety & Emergency Needs

The most overlooked component of SIP planning is the emergency fund.

Most people either:

- Keep too much idle cash, or

- Invest emergency money in risky assets

Both are dangerous.

Liquid funds provide:

- High liquidity

- Very low volatility

- Better efficiency than savings accounts in most cases

In practical terms, money needed within one year should never be exposed to market risk. This is why the 1-year rule is non-negotiable.

Why the 7-5-3-1 Rule Is Considered a Safe Wealth-Creation Formula

The strength of this rule lies in time-based risk reduction.

Instead of reacting emotionally to market movements, you follow a predefined structure. This removes guesswork and impulsive decisions.

Most people don’t realise that panic selling destroys more wealth than bad fund selection. A rule-based SIP framework prevents this.

The 7-5-3-1 rule helps by:

- Reducing emotional investing

- Improving financial discipline

- Protecting short-term goals

- Allowing equity to work long term

This is why it is widely considered a safe SIP investment strategy.

SIP Example Using the 7-5-3-1 Rule (Indian Scenario)

Monthly SIP Allocation Example

Let us take a ₹25,000 monthly SIP as an example:

- ₹10,000 → Equity SIP (7+ year goals)

- ₹7,000 → Hybrid SIP (5-year goals)

- ₹5,000 → Debt SIP (3-year goals)

- ₹3,000 → Liquid fund (emergency buffer)

This structure ensures no single market event can derail your entire financial plan.

What Happens During Market Ups and Downs

When markets fall sharply:

- Equity SIPs accumulate more units

- Hybrid funds reduce volatility

- Debt and liquid funds remain stable

This balance keeps investors invested long enough to benefit from compounding.

Expected Returns from the 7-5-3-1 SIP Rule

One truth must be stated clearly: there are no guaranteed returns in mutual fund investing.

However, realistic long-term expectations are:

- Equity SIPs (7+ years): 11–14% CAGR over full cycles

- Hybrid SIPs (5 years): 8–10% CAGR

- Debt SIPs (3 years): 6–7% CAGR

- Liquid funds (1 year): Stability + liquidity

The real magic happens through compounding over time, not short-term performance.

Who Should Follow the 7-5-3-1 Rule in SIP

This rule is especially suitable for:

- First-time SIP investors

- Salaried employees

- Risk-conscious individuals

- Long-term financial planners

If your priority is financial security rather than speculation, this rule fits well.

Who Should Modify or Avoid the 7-5-3-1 Rule

Aggressive investors with:

- High income stability

- Strong market understanding

- High risk tolerance

may increase equity exposure. However, even seasoned investors usually respect the 1-year and 3-year rules.

7-5-3-1 Rule vs Traditional SIP Strategy

Rule-Based SIP vs Random SIP Investing

Traditional SIPs often rely on:

- Past returns

- Star ratings

- Market trends

Rule-based SIPs focus on:

- Time horizon

- Risk-adjusted returns

- Emotional control

From long-term experience, rule-based investing consistently reduces stress and improves outcomes.

Common Mistakes While Following the 7-5-3-1 Rule

- Choosing wrong fund categories

- Expecting fixed or guaranteed returns

- Ignoring annual rebalancing

- Stopping SIPs during market corrections

These mistakes quietly erode long-term wealth.

How to Start SIP Using the 7-5-3-1 Rule (Step-by-Step)

Step 1 – Identify Financial Goals by Time Horizon

List goals clearly with realistic timelines.

Step 2 – Select Appropriate Mutual Fund Categories

Do not mix equity with short-term goals.

Step 3 – Decide SIP Amount and Start Investing

Consistency matters more than amount.

Step 4 – Review and Rebalance Annually

Adjust allocations as goals approach.

Tax Impact Under the 7-5-3-1 SIP Rule (India)

- Equity funds are taxed based on holding period

- Debt funds are taxed as per prevailing rules

- Holding discipline improves tax efficiency

Tax should never drive investment decisions, but it must be understood.

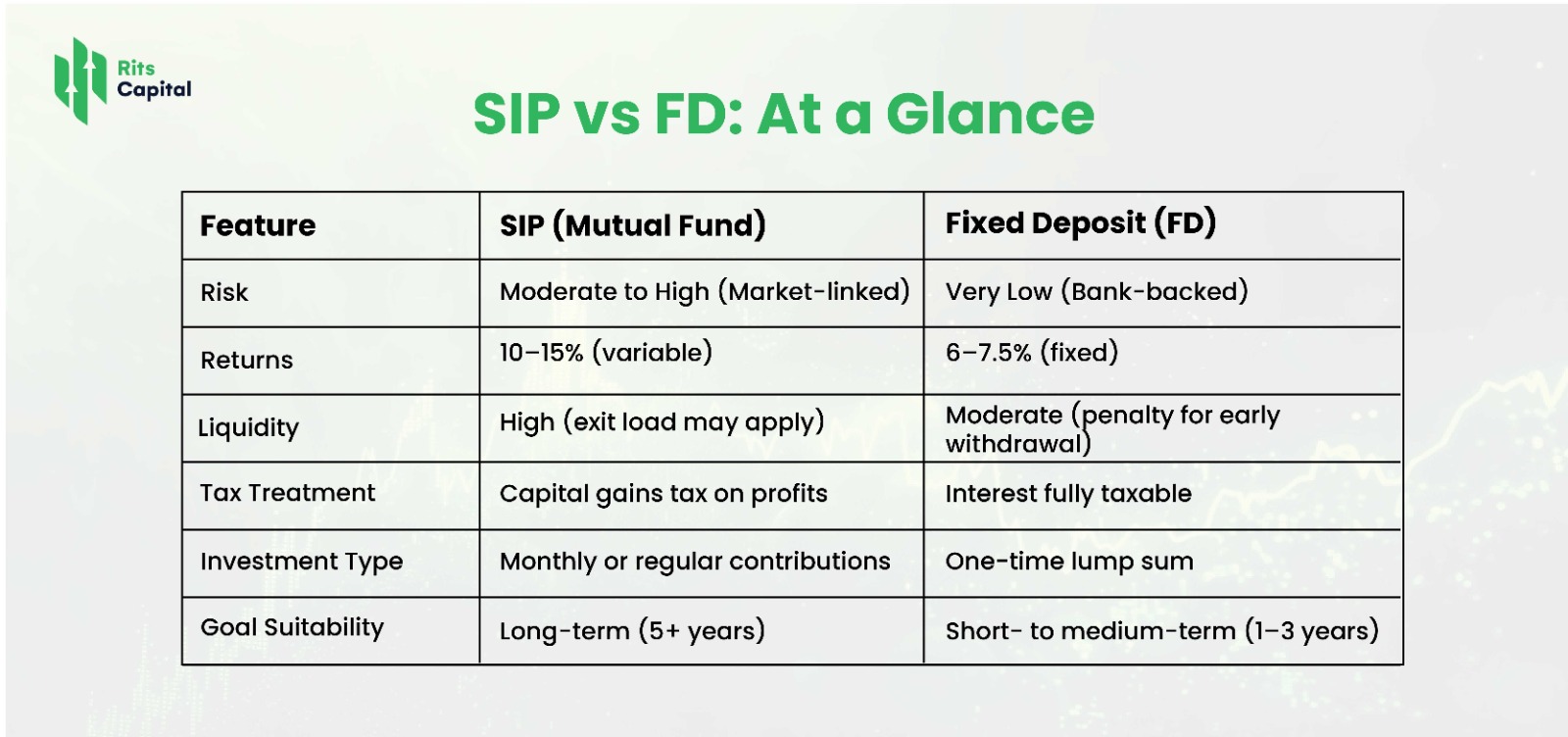

7-5-3-1 Rule vs Fixed Deposit and RD

FDs offer certainty but struggle against inflation. SIPs, when structured correctly, aim for real wealth creation.

FAQs – 7-5-3-1 Rule in SIP

Is the 7-5-3-1 rule safe during market crashes?

Yes, the 7-5-3-1 rule is considered relatively safe during market crashes because it spreads investments across different time horizons and asset classes. Long-term equity SIPs benefit from market recoveries, while hybrid, debt, and liquid funds provide stability, liquidity, and protection for short- and medium-term goals.

Can beginners use the 7-5-3-1 SIP rule?

Yes, beginners can confidently use the 7-5-3-1 SIP rule. It is designed to be simple and time-based, making fund selection easier for first-time investors. By matching investment duration with the right asset type, beginners can reduce risk, avoid emotional mistakes, and build wealth steadily through disciplined SIP investing.

Is the 7-5-3-1 rule suitable for retirement planning?

Yes, the 7-5-3-1 rule is well-suited for retirement planning when applied correctly. Retirement goals typically have long time horizons, making the 7-year equity component ideal for growth. As retirement approaches, shifting gradually to hybrid and debt funds helps reduce risk and protect accumulated wealth.

How often should SIPs be reviewed under this rule?

Under the 7-5-3-1 rule, SIPs should ideally be reviewed once a year. An annual review is enough to check goal progress, rebalance asset allocation, and adjust SIP amounts if income or timelines change. Frequent reviews often lead to emotional decisions and unnecessary fund switching, which can hurt long-term returns.

What is the 7-5-3-1 rule for SIP investments?

The 7-5-3-1 rule for SIP investments is a time-based strategy that matches investment duration with fund type. Equity funds are used for 7+ years, hybrid funds for 5 years, debt funds for 3 years, and liquid funds for 1 year, helping reduce risk and improve financial discipline.

What is the 7-5-3-1 rule?

The 7-5-3-1 rule is an investment planning framework that aligns money with its time horizon. It prevents short-term money from being exposed to high market risk and allows long-term investments to benefit from equity growth, making it a safer and more structured approach to wealth creation.

How to become rich through mutual fund SIPs?

To build wealth through mutual fund SIPs, focus on long-term investing, disciplined monthly contributions, correct asset allocation, and patience during market volatility. Consistently investing for 10–15 years, choosing funds based on time horizon, and avoiding panic withdrawals are more important than chasing high-return funds.

How to maximise your investment in mutual fund SIPs?

You can maximise SIP returns by staying invested long term, increasing SIP amounts with income growth, aligning funds with goals, rebalancing annually, and avoiding frequent switches. Time in the market, compounding, and emotional control matter far more than trying to time market highs and lows.

Final Verdict – Should You Use the 7-5-3-1 Rule in SIP?

From what I have seen in real-world investing, the biggest challenge for most SIP investors is not fund selection or market timing—it is behaviour. People abandon SIPs during market falls, overinvest in equity for short-term goals, or expect fixed returns from market-linked products. This is exactly where the 7-5-3-1 rule proves its value.

In practical terms, the 7-5-3-1 rule brings structure to uncertainty. By linking each rupee of your SIP to a clear time horizon, it ensures that short-term needs are protected, medium-term goals are balanced, and long-term goals are given enough time to grow. This alignment significantly reduces panic selling during market crashes because not all your money is exposed to equity risk at the same time.

Most people don’t realise that wealth is rarely destroyed by markets—it is destroyed by emotional decisions made during volatility. The 7-5-3-1 rule counters this by enforcing financial discipline. Equity SIPs are allowed to compound over long periods, while hybrid, debt, and liquid funds act as shock absorbers when markets turn volatile or interest rates change.

That said, this rule is not a guarantee of returns and should not be treated as a rigid formula. It is a guiding framework. Investors with higher risk appetite or changing income patterns may need to modify allocations over time. Regular annual reviews and rebalancing remain essential.

For beginners, salaried professionals, and long-term planners in India, the 7-5-3-1 rule offers a practical, low-stress, and sensible approach to SIP investing. Used with patience and consistency, it does not promise extraordinary gains—but it greatly improves the chances of achieving stable, long-term financial security without regret.